2017 San Diego Lodging Forecast

Regional Economy

San Diego is known for its mild year-round climate, tourist attractions, Convention Center, U.S. Navy and its more recent developments as a healthcare, biotechnology and communications technology development center. San Diego County has a population of 3.3 million and the city of San Diego has 1.3 million residents. It’s quality of life, coupled with the education sector (University of California, San Diego State University and University of San Diego) as well as others provide the foundation for much of the growth in biotechnology and telecommunications industries. Potentially, we could add a cybersecurity industry here and we are well-positioned for future economic prosperity in many areas.

San Diego County added 41,400 jobs, increasing its job base to 1.39 million in 2015. This amounts to a 3.1 percent annual growth rate that when the final numbers come in, should be strong in 2016 as well. The economy is on firm ground and is no longer solely a military town. It is these strengths that create an opportunity for San Diego to have a powerful tourism industry presence that includes strong group, leisure and corporate lodging demand year around.

Lodging Sector

To provide some historical perspective, San Diego’s occupancy and average rates have been growing steadily as can be seen from the chart below that depicts occupancy, average rate and revenue per available room (RevPAR). San Diego benefits from having a “drive” market so it does not typically get hit as hard as other major markets that rely on air traffic. The bottom of the market for other cities was 10 points below San Diego’s 66 percent performance in 2010.

| Year | Occupancy | ADR | RevPAR |

| 2010 | 66% | $122 | $81 |

| 2011 | 69% | $126 | $87 |

| 2012 | 71% | $132 | $93 |

| 2013 | 72% | $136 | $97 |

| 2014 | 75% | $142 | $106 |

| 2015 | 76% | $151 | $115 |

| 2016 | 77% | $155 | $119 |

| 2017 (forecast) | 77% | $160 | $123 |

In 2017, San Diego will maintain the highest occupancy levels in the last 30 years achieved in 2016 and it will reach the highest average rates ever. However, the resultant revenues will not provide for the highest net income ever recorded because operating costs have been rising beyond inflation mostly as the result of increased labor and benefit costs stemming from the increases in minimum wages and sick leave ordinances. Following is a review of 2016 and a forecast for 2017. While 2017 and 2018 will add new hotel supply beyond that of 2016, San Diego will remain a strong market for the foreseeable future and should be able to hold the overall 77 percent occupancy for the next few years.

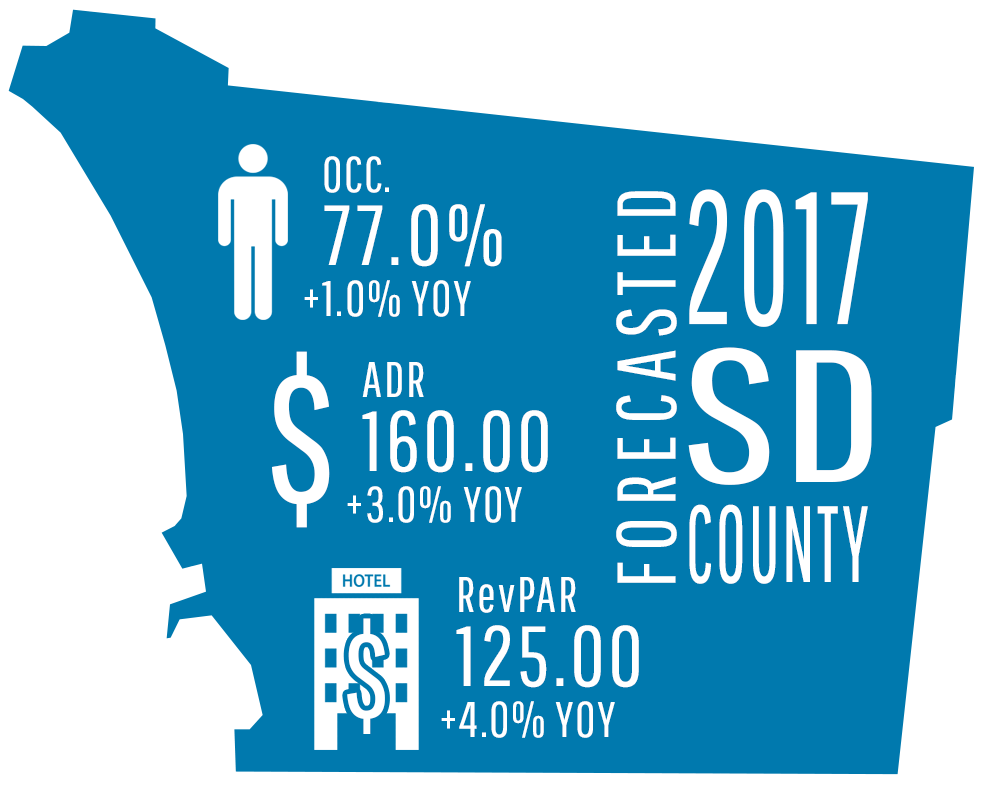

San Diego County

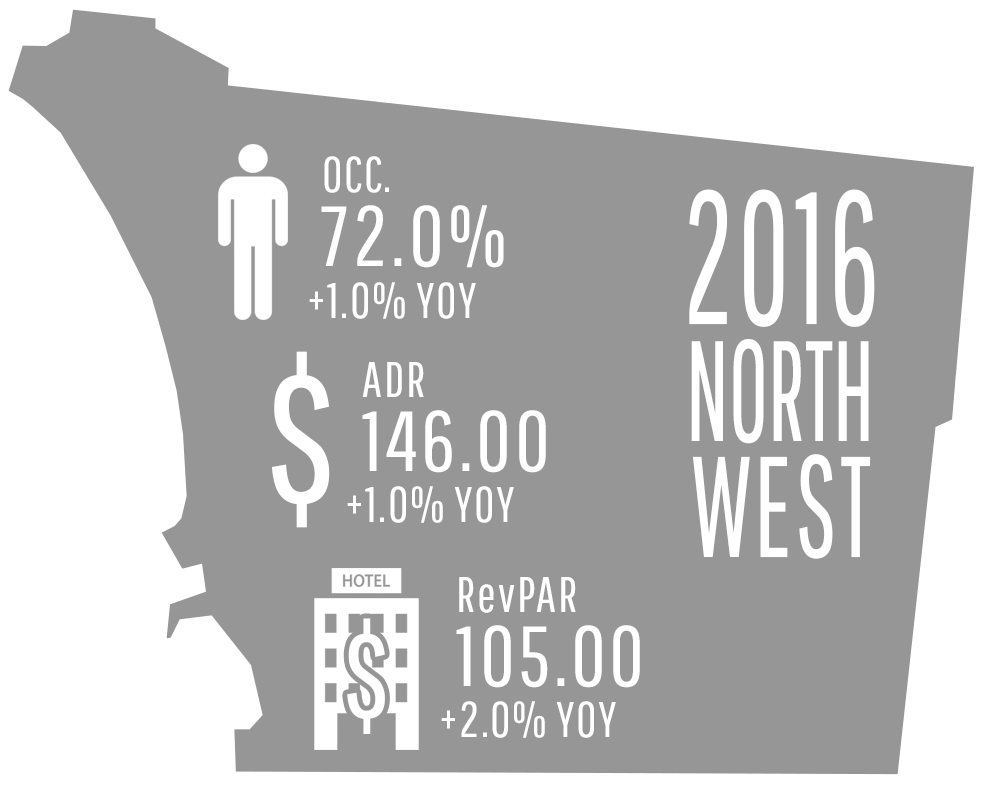

In 2016, occupancy in San Diego County increased 1 percent to 77 percent and average rate grew 3 percent to $155. Revenue per available room (RevPAR) moved up 4 percent to $120. New hotels that were added in 2016 included 1,017 rooms but based on their opening dates, the 2016 impact was less as indicated below; the 2017 impact of properties opening (or already opened) this year is also listed below.

| Hotels Opened in 2016 | Rooms | Impact in 2016 |

| Springhill Suites Downtown | 253 | 42 |

| Residence Inn Downtown | 147 | 25 |

| Springhill Suites Mission Valley | 135 | 23 |

| Homewood Suites Downtown | 160 | 93 |

| Hilton Garden Inn Downtown | 204 | 119 |

| Homewood Suites San Diego Mission Valley/Zoo | 118 | 30 |

| TOTAL | 1,017 | 332* |

| * plus 378 from hotels opened in 2015 for a total of 710. | ||

| Hotels Opening in 2017 | Rooms | Impact in 2017 |

| Pendry Hotel Downtown | 317 | 317 |

| Fairfield Inn & Suites San Diego North/San Marcos | 116 | 87 |

| Springhill Suites Carlsbad | 103 | 9 |

| Homewood Suites San Diego Hotel Circle/Sea World | 245 | 143 |

| Residence Inn Chula Vista | 148 | 74 |

| Courtyard by Marriott El Cajon | 115 | 86 |

| TOTAL | 1,044 | 716 |

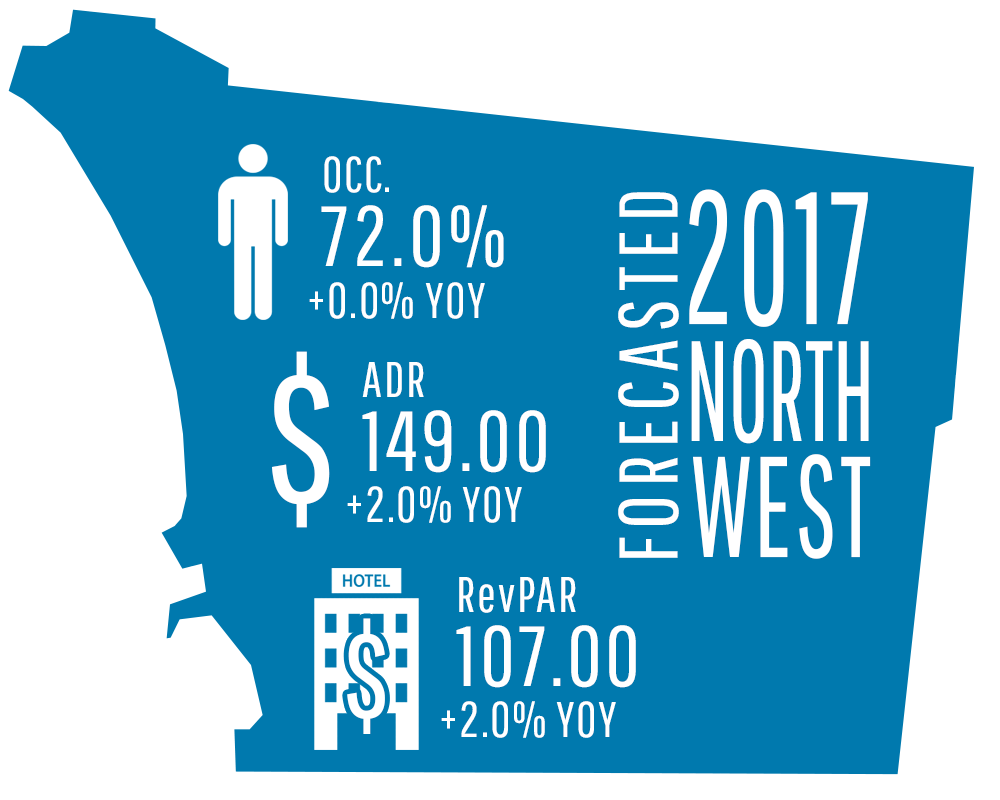

As a result, the impact from these hotels will be 716 new rooms for 2017. Given that this represents 1.2 percent new supply in the County this year, in 2017 we expect occupancy levels to remain at 77 percent with average rate growth of 3 percent to $160 and RevPAR of $125. This new supply increase will be absorbed by demand increases at the same level or higher. Rates will grow based on the number of sellout nights in the market, the negotiated rates during the request for proposal (RFP) season, the rates on the books according to TravelClick, Convention Center room nights and other sources. While there are a number of hotels opening in 2018 and beyond, this supply increase is rather muted compared to New York, Los Angeles and many other U.S. cities.

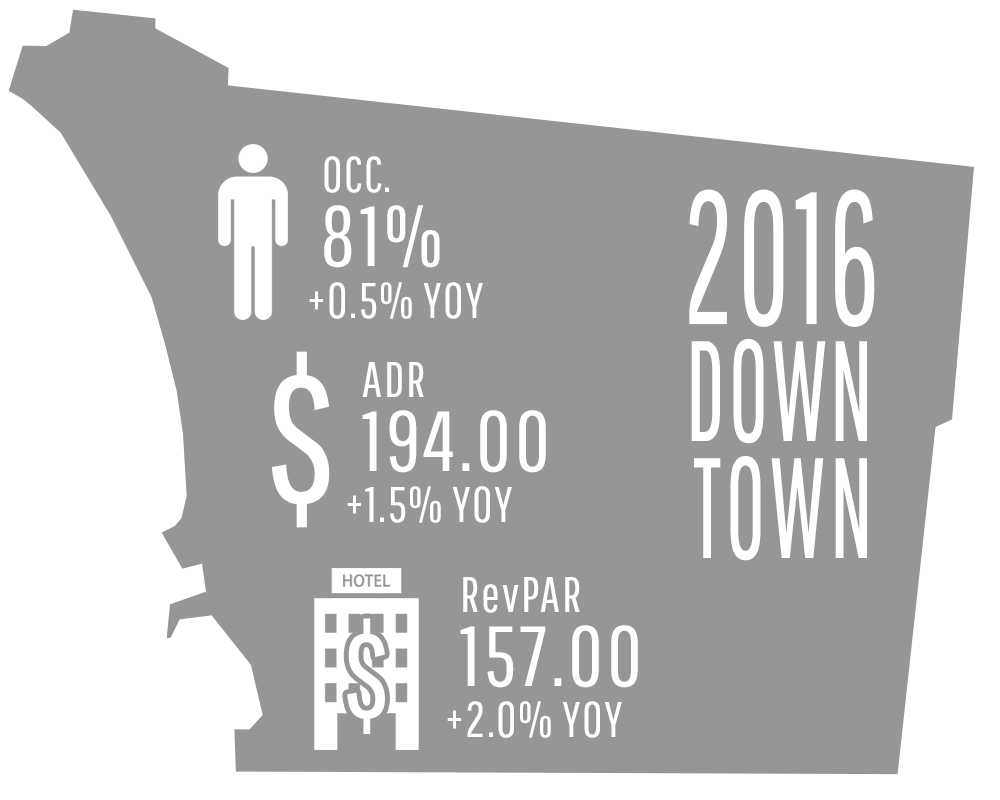

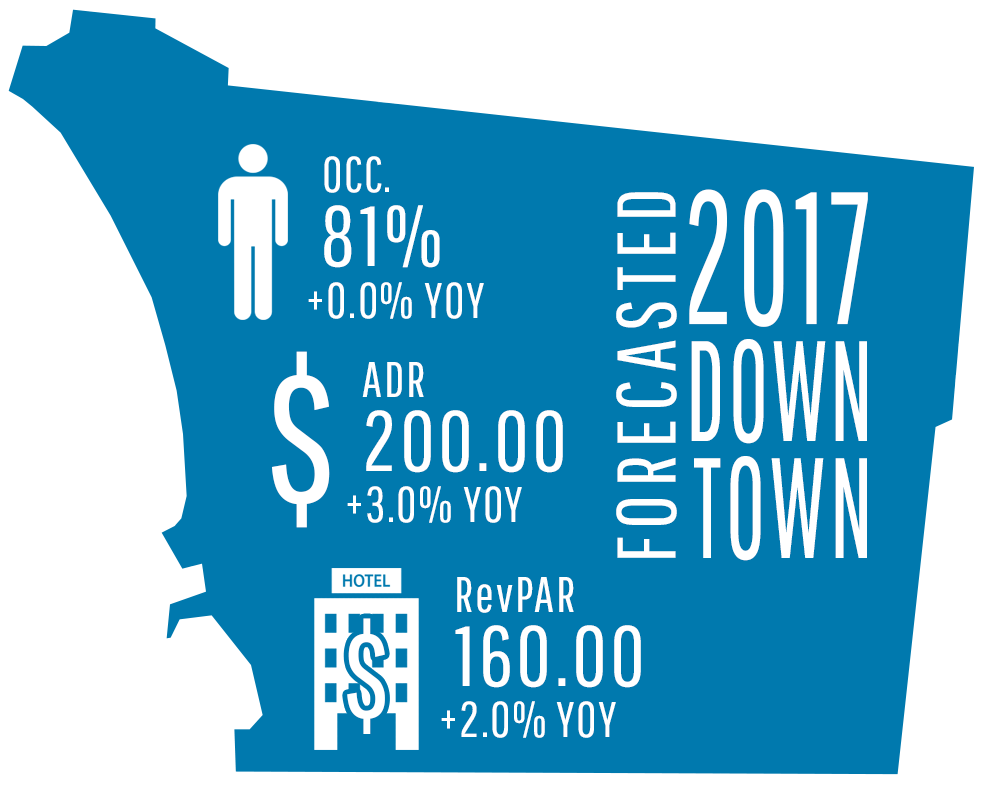

Downtown

2017 will bring additional hotel construction as well as strong convention center demand due to strong cyclical bookings by the San Diego Tourism Authority but the only new Downtown hotel opening was the 317 Pendry Hotel that opened in January. New supply will be up 5 percent but demand will increase by nearly 5 percent, holding occupancy levels at 81 percent. Average rates will continue to grow due to the number of sellout nights and some compression from a few notable citywide conventions from $194 to $200, up 3 percent. RevPAR will increase 3 percent to $160.

2017 Total: 317 total rooms plus those impacting 2017 but opened in 2016 is 592 or just over 3 percent of supply. Note: We anticipate that Airbnb will have a significant impact on average rates during peak periods, however, the overall annualized impact will be minimal in 2017.

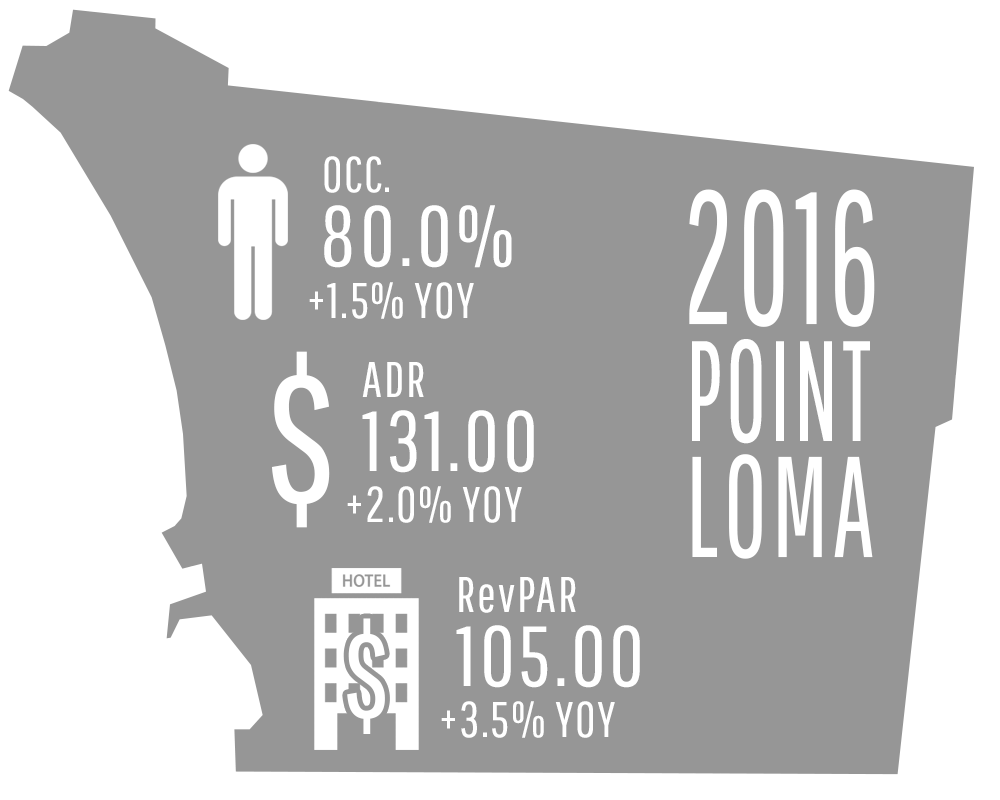

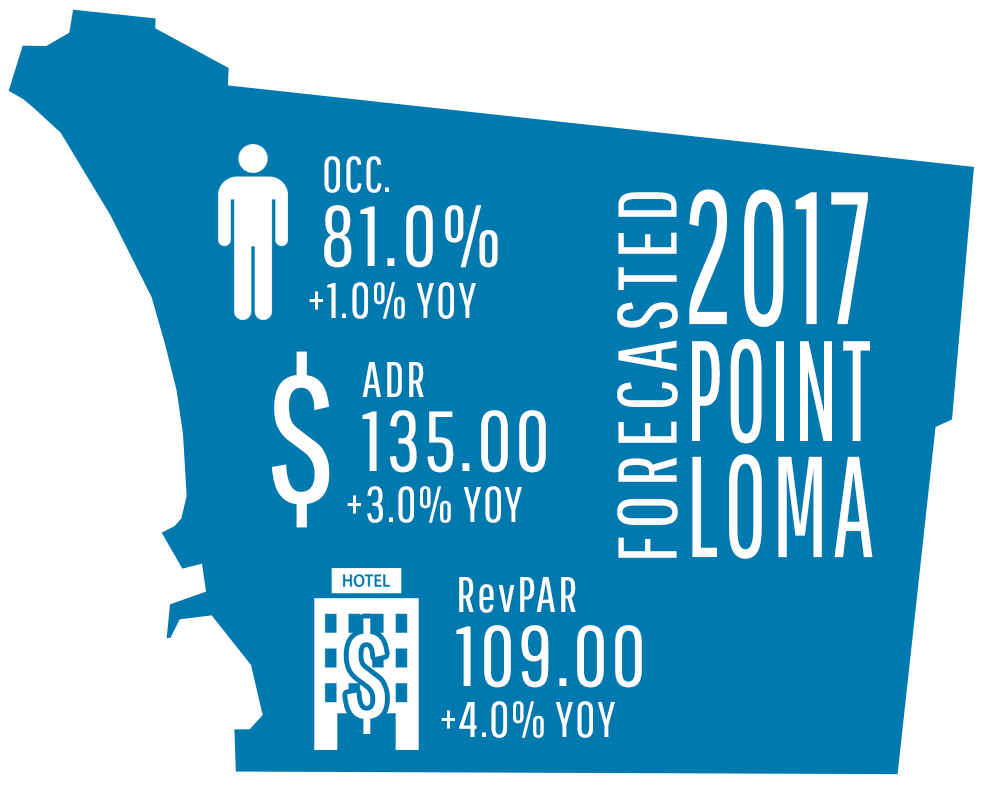

Point Loma Peninsula

Occupancy levels will increase by 1 percent to 81 percent due to no new supply in 2017 and rates should grow at 3 percent to hit $135. Point Loma rooms added in 2017: None but several are in planning.

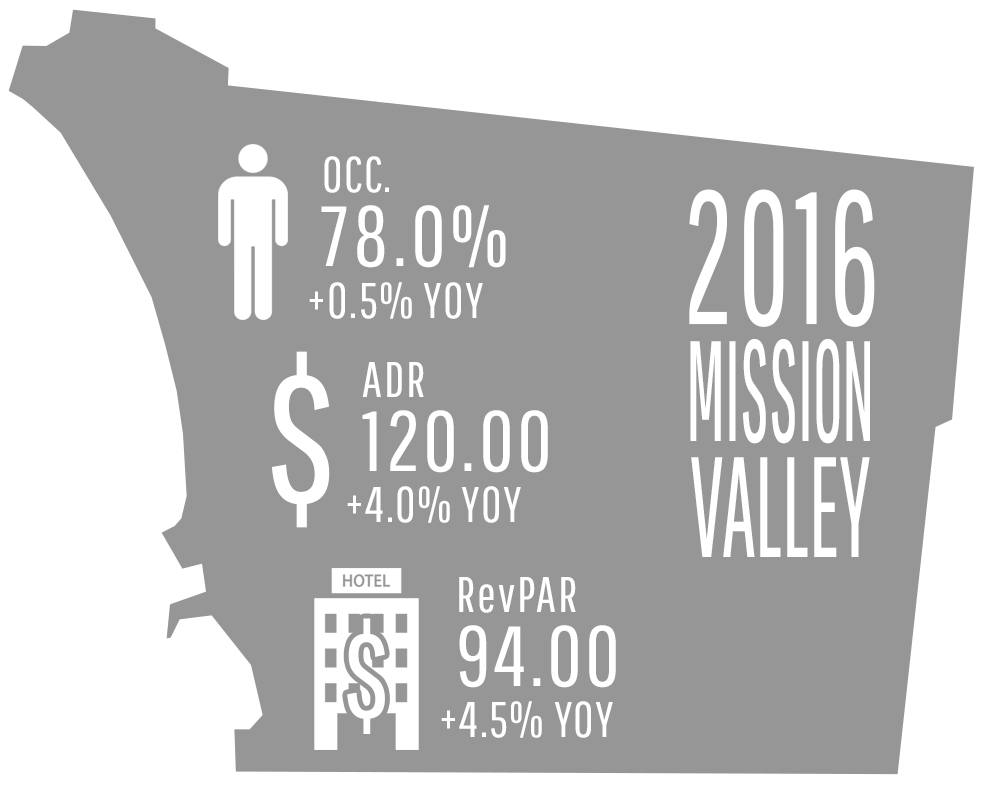

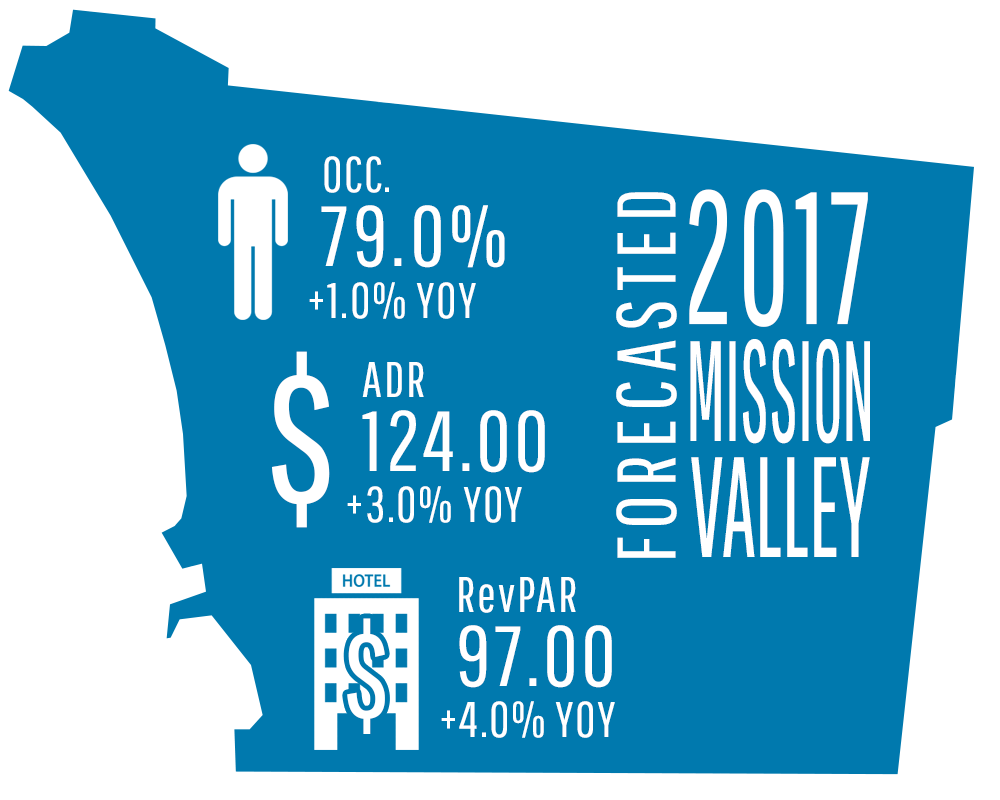

Mission Valley

In 2017, the Homewood Suites San Diego Hotel Circle/Sea World Area will add 245 rooms to Mission Valley with an impact of 143 rooms. Demand will exceed this near zero new supply to boost occupancy to 79 percent with rates up 3 percent to $124. RevPAR will increase 4 percent to $97.

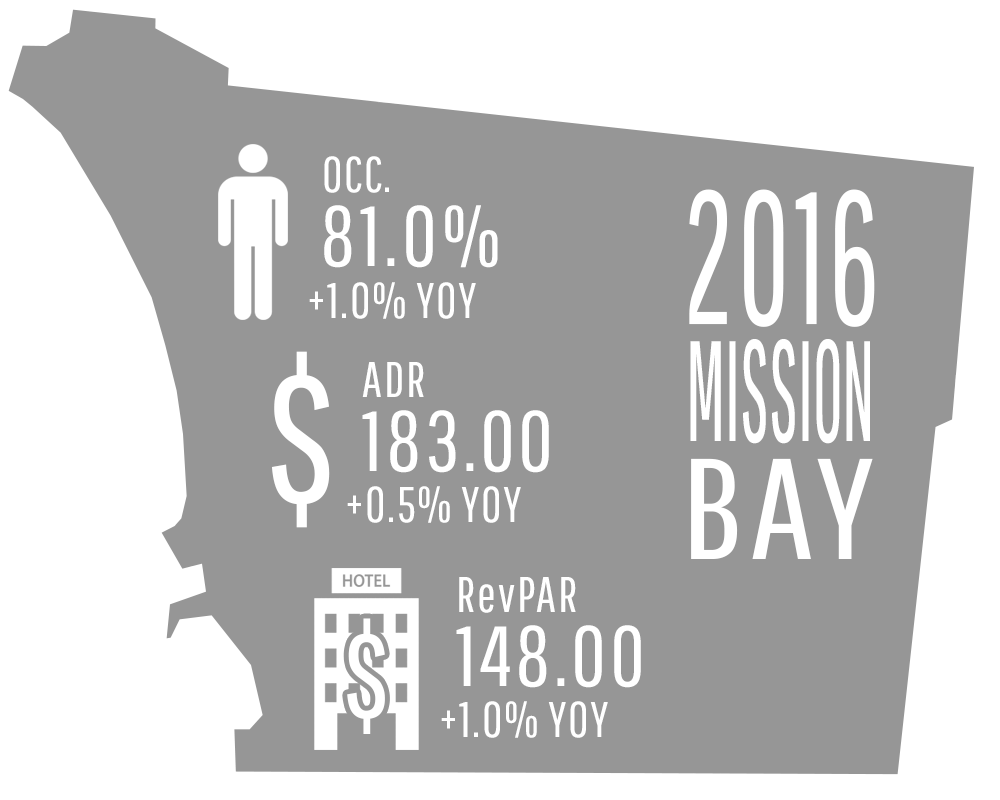

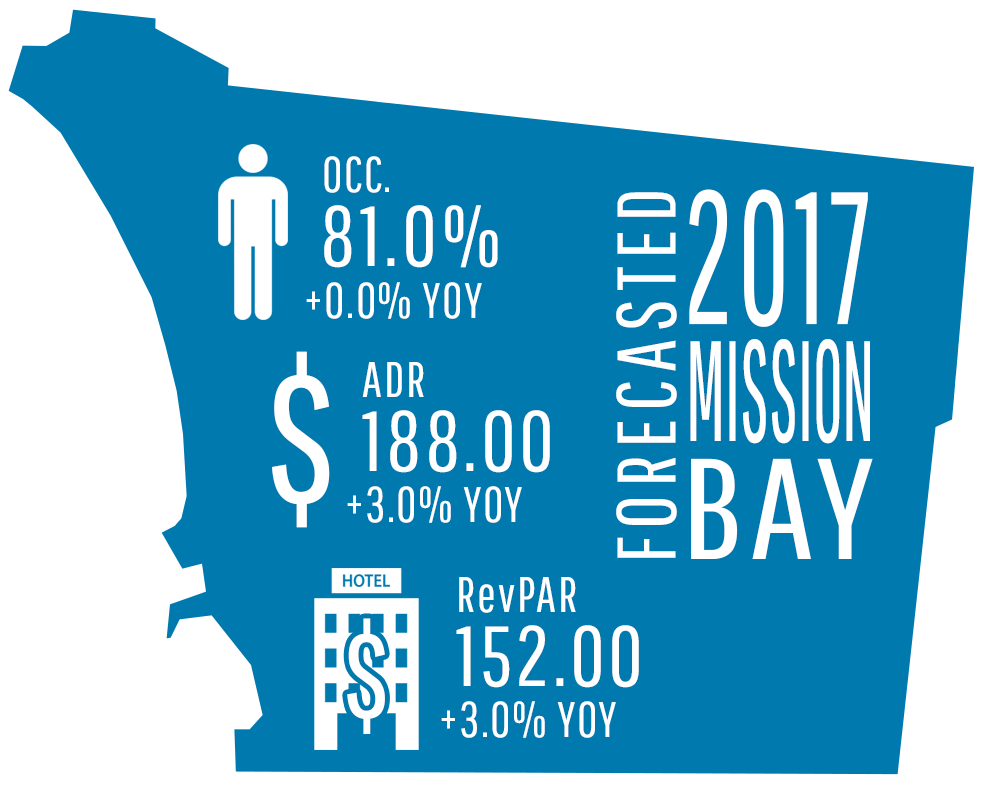

Mission Bay

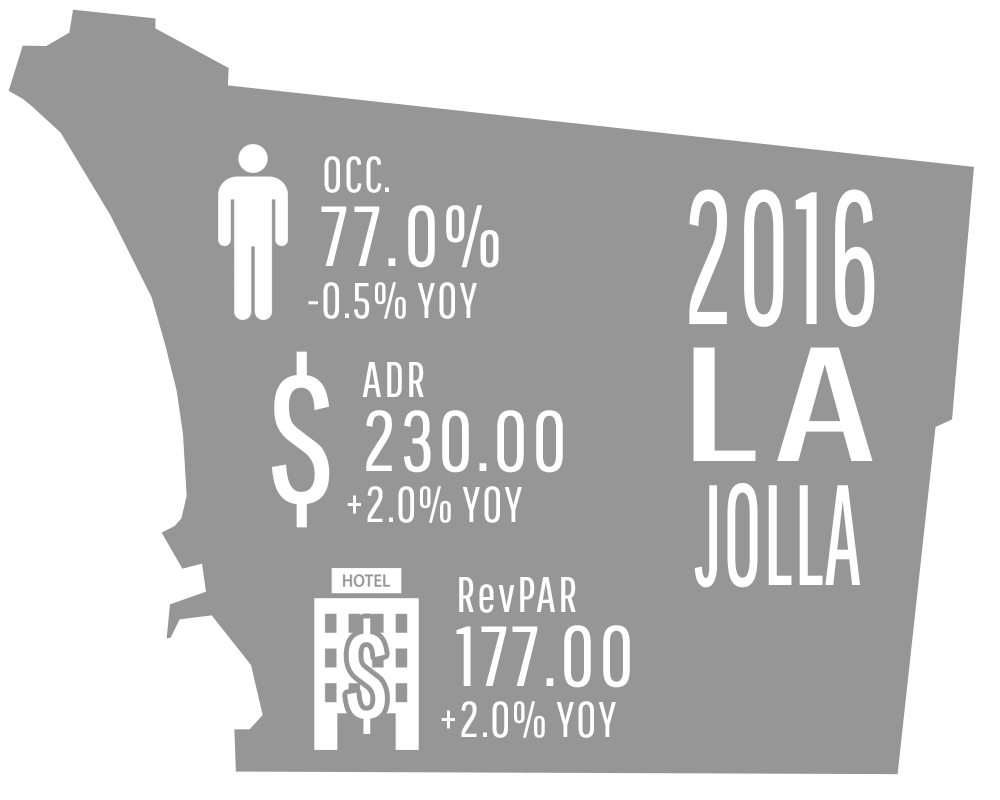

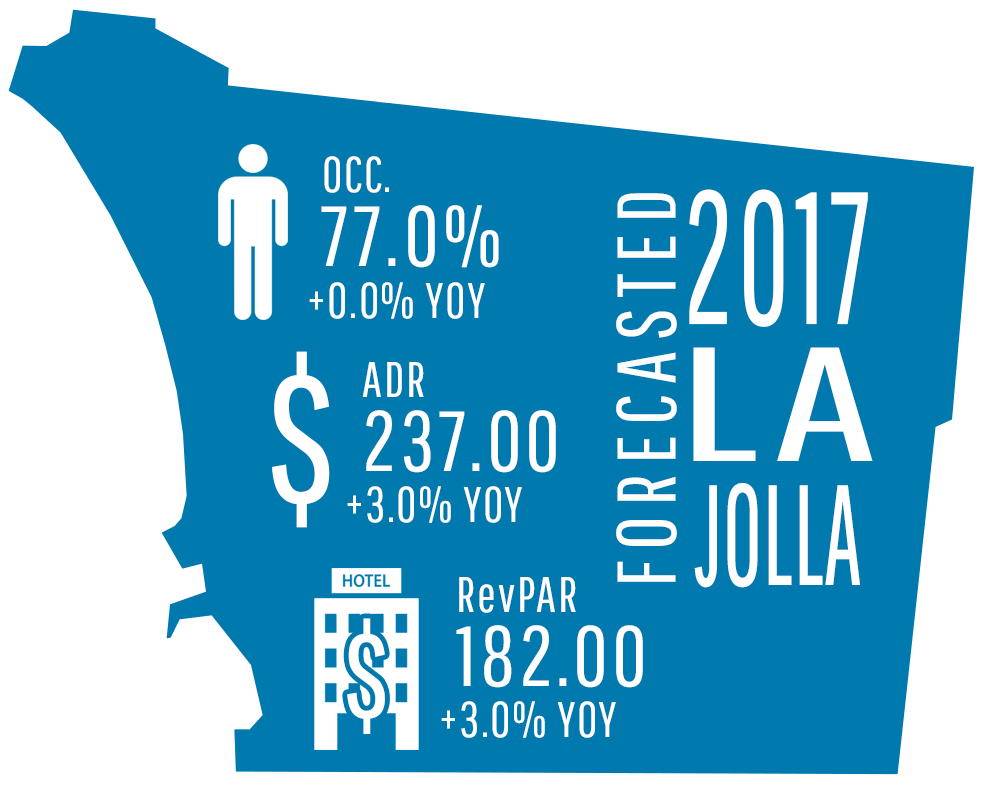

La Jolla

With no new supply, this

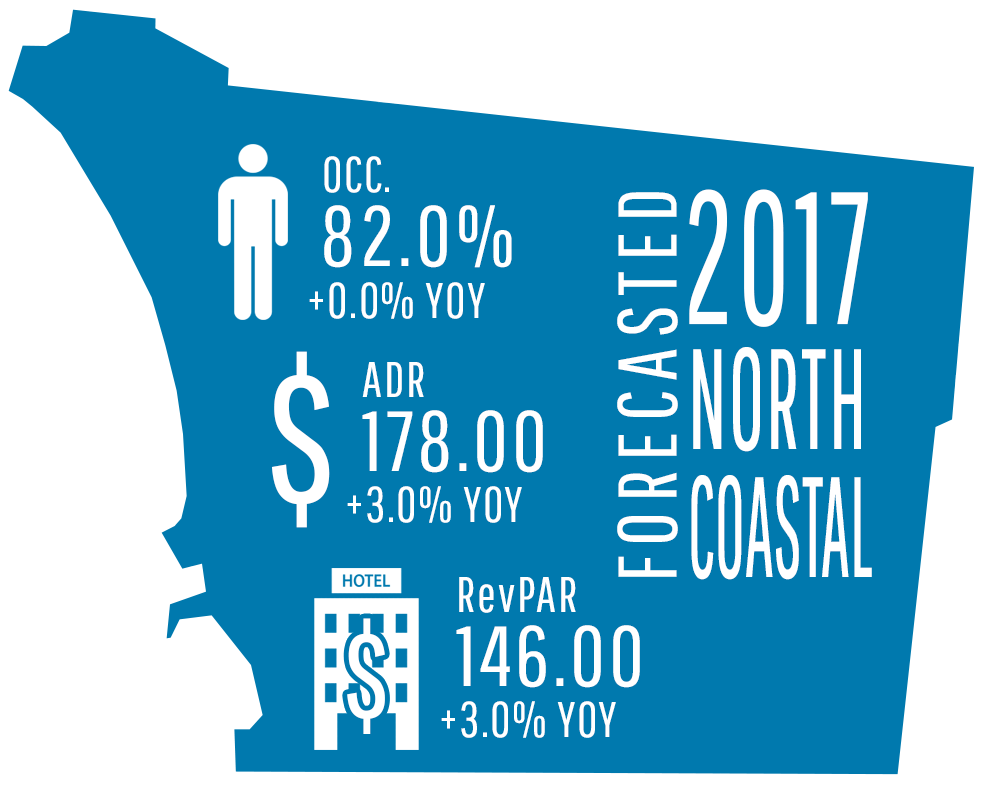

North Coastal

Half the hotels are full-service and the other half

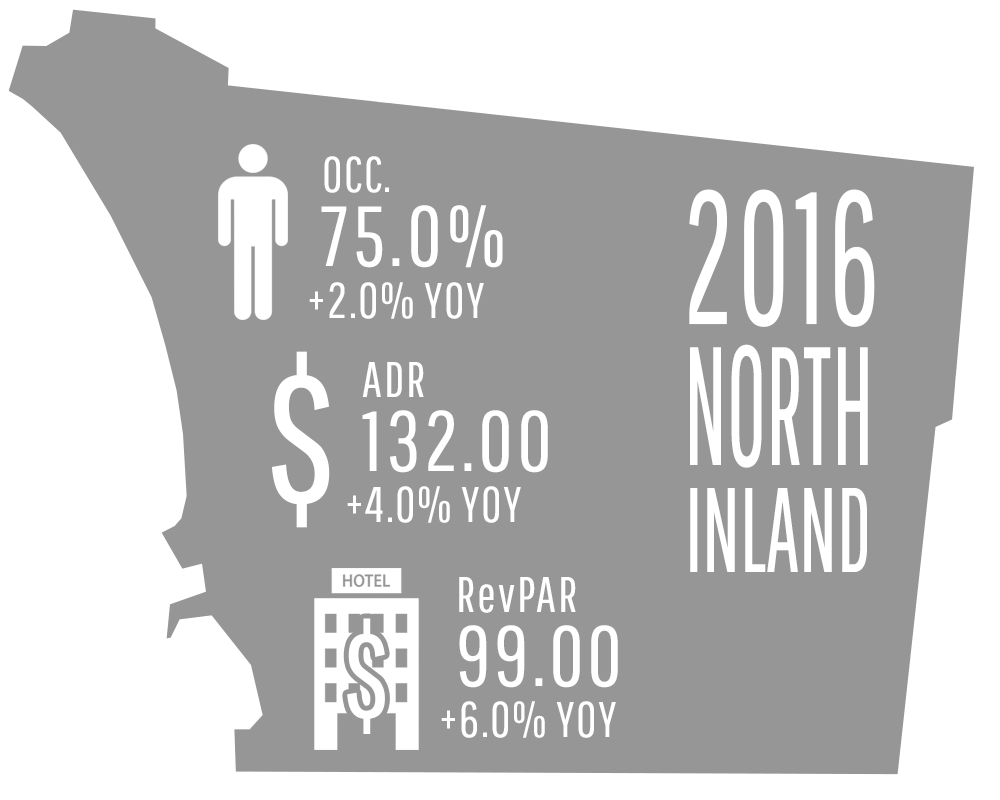

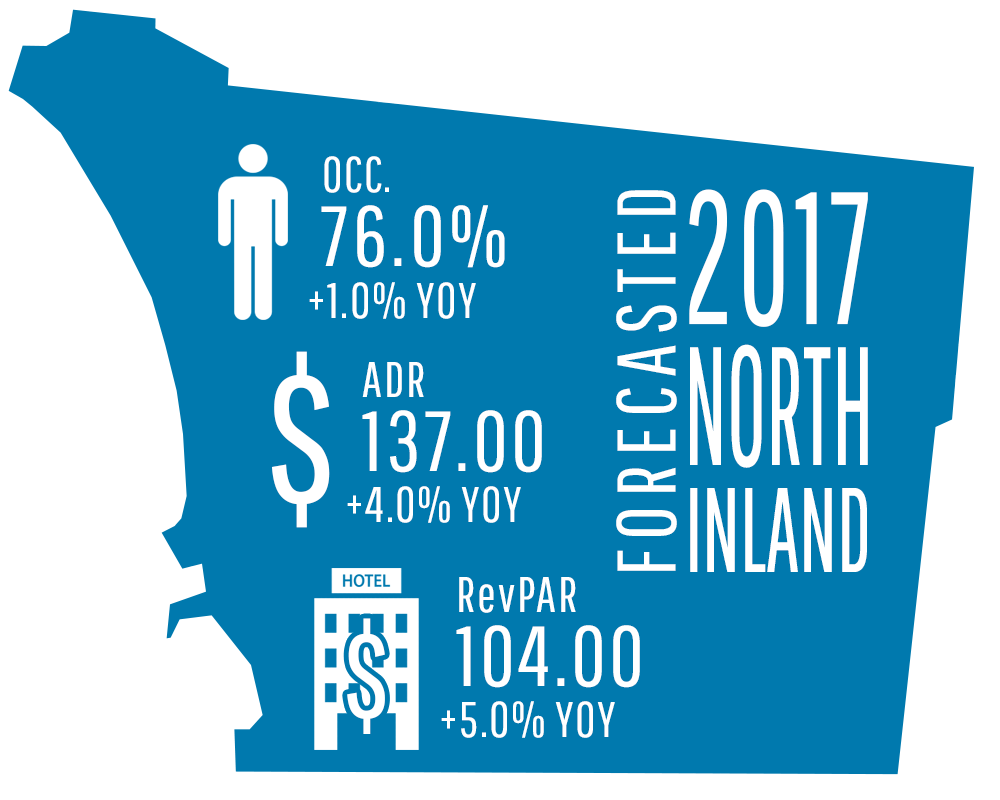

North Inland

Corporate business is solid with numerous industrial parks and Sharp Rees-Stealy adds 100,000 square feet of medical. Palomar Community College South Education Center opens next year and this submarket continues to perform well.

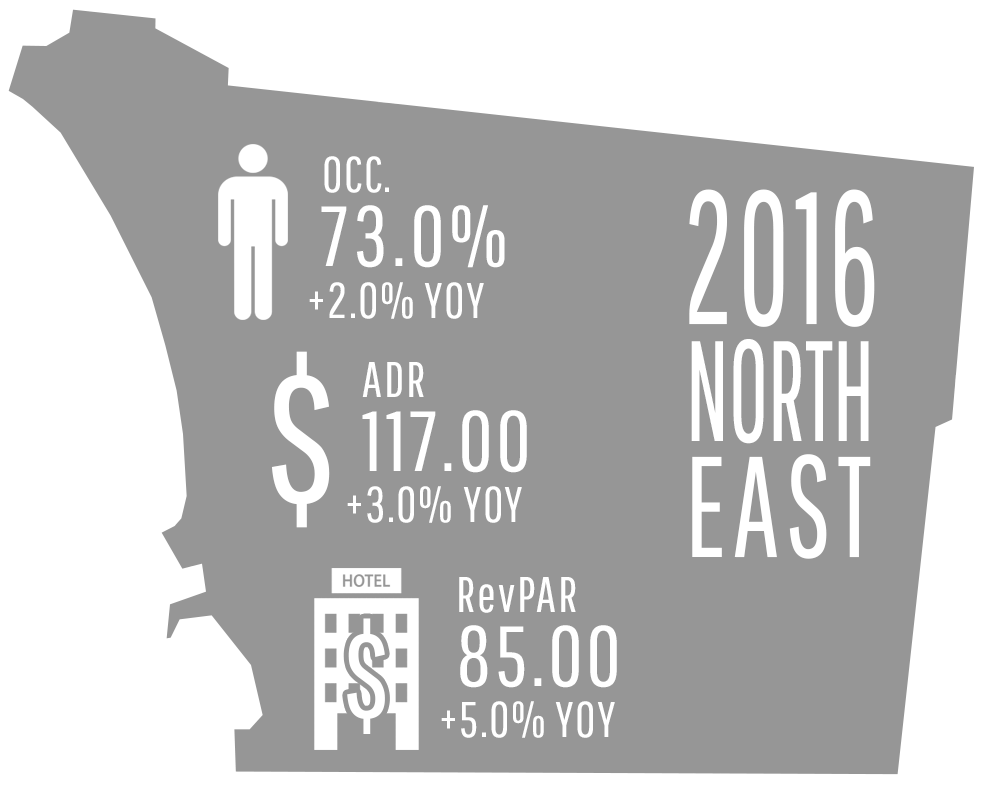

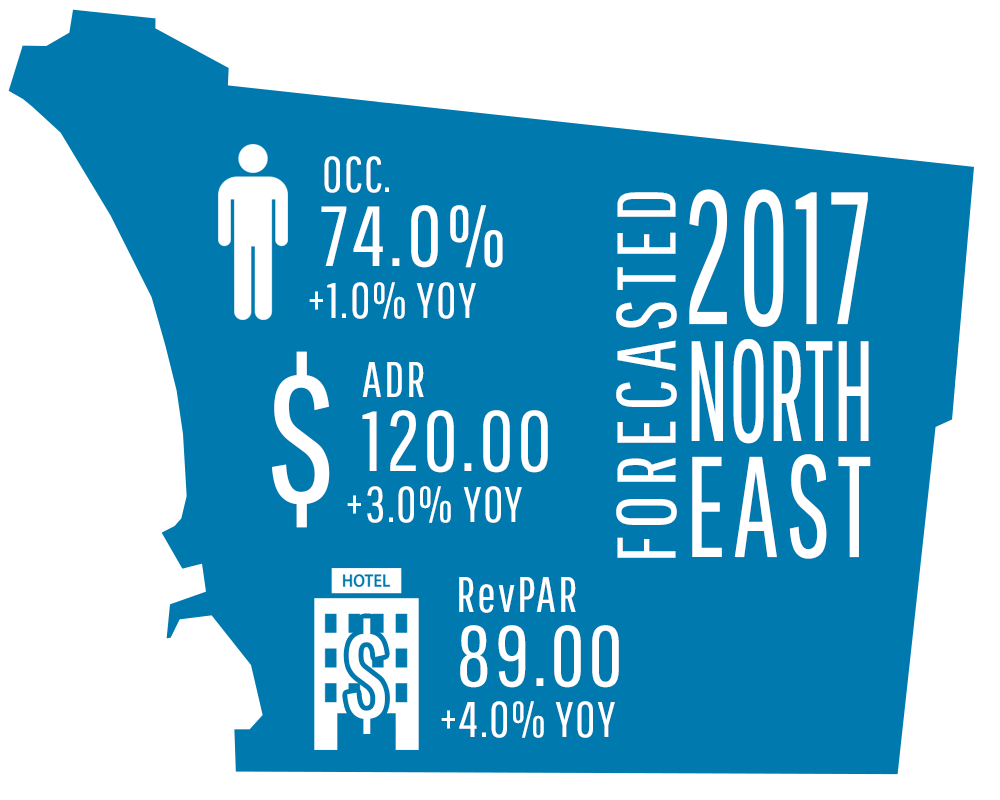

Northeast

In 2017, this area will see occupancy levels increase one point to 74 percent, average rates grow 3 percent to $120, and RevPAR up 4 percent to $89. The SR-78 corridor, coupled with the growth of California State University San Marcos, Palomar Community College, Pima Medical Institute and other health care facilities and population growth make this an area that is both desirable and will see more new supply over the next two years. Escondido brings Innovation and Victory Park this year, Stone Brewery is building a hotel soon and our Fairfield Inn & Suites San Diego North/San Marcos opens next month. Vista sports 13 breweries, the most per capita of any U.S. city.

Northwest

Oceanside has finally blossomed into a force with solid leisure demand and amenities that include a new Oceanside High School Performing Arts Center, 1,000 slip harbor, airport, San Luis Rey Mission and Mira Costa College. The area has seen massive increases in supply over the past few years and has absorbed this supply well as Carlsbad continues to have a deep reservoir of industrial and corporate demand generators including ViaSat and ThermoFisher Scientific. LEGOLAND California, Carlsbad Premium Outlets and Carlsbad’s downtown Village provide strong leisure demand. Having said that, the supply of limited-service hotels needs to slow as demand cannot continue to keep the pace of recent supply growth.

Events in San Diego in 2017

In January, San Diego hosted the Farmers Insurance Golf Tournament that was a big success. The World Baseball Classic just finished up with an estimated 5,000 room nights, the Red Bull Air Races are coming up in April with the potential for close to 10,000 room nights and the Gold Cup Soccer Tournament in July is estimated to generate 10,000 room nights. KAABOO Del Mar in September has become quite the music extravaganza and will also drop thousands of room nights into the market, Extreme Sailing in October will likely hit 10,000 room nights and the Breeder’s Cup in November will be “huge!” (I know, quoting a president doesn’t always work).

Looking back on 2016, the Chargers left but gave us an opportunity to develop the Qualcomm site, promote tourism and conventions rather than football (there is a large delta between the marginal economic impact of football versus the massive economic impact of conventions) and perhaps helping our city with solving challenges like homelessness. Good riddance to the Chargers (we’ll find plenty to cheer about in San Diego without them). Having said that, I’m still rooting for Rivers and Gates and all the players—the ownership left us and time will tell how they do in L.A.